E-Invoicing

This category is to group E-Invoicing articles together

- Details

- Written by: Administrator

- Category: E-Invoicing

- Hits: 9

I would like to invite you and your colleagues to attend the In-Person Seminar - Implementation Strategies for E-Invoicing on May 24, 2024 (Friday) [09:00 ~ 17:00] at Eastin Hotel, Petaling Jaya. Total 7.0 hours seminar.

In this seminar, we will include a session to discuss proper implementation strategies for e-invoicing in Malaysia. We will also discuss gap assessment analysis on e-invoicing based on the latest updates from the tax authority. If there is any feedback on the result of sand box testing and pilot run that is scheduled in the month of May 2024, we will address the critical issues in this seminar as well.

Here are the top nine reasons why it is important to attend this workshop:

Please download the training flyer via the download link or register using Online Form:

In-Person Seminar - Implementation Strategies for E-Invoicing

You can scan the QR Code to download to your mobile device using Wechat or QR Scanner.

- Details

- Written by: Administrator

- Category: E-Invoicing

- Hits: 12

I would like to invite you and your colleagues to attend the online seminar - Implementation Strategies for E-Invoicing on May 28, 2024 (Tuesday) [09:00 ~ 17:30]. Total 7.5 hours online seminar.

In this online seminar, we will include a session to discuss pragmatic implementation strategies for e-invoicing in Malaysia. We will also discuss gap assessment analysis on e-invoicing based on the latest updates from the tax authority. If there is any feedback on the result of sand box testing and pilot run that is scheduled in the month of May 2024, we will address the critical issues in this seminar as well.

Here are the top nine reasons why it is important to attend this workshop:

Please download the training flyer via the download link or register using Online Form:

Online Seminar - Implementation Strategies for E-Invoicing

You can scan the QR Code to download to your mobile device using Wechat or QR Scanner.

- Details

- Written by: Administrator

- Category: E-Invoicing

- Hits: 460

E-Invoicing Study: Anticipated Components in Software Development Kit - System Specification

This article is trying to highlight the anticipated contents inside Software Development kit before the official document is scheduled to release in December 2023 or any time after the article publication.

The software development kit shall consider of the following sections:

- Digital Certificate and Signature

- IRBM announced in the guideline that digital signature is embedded into the e-invoice. Therefore, IRBM shall use Tax Identification Number to create the digital certificate for specific taxpayer as an authentication approach to validate the identity of the taxpayer. The SDK shall indicate a digital signature to be embedded in the e-invoice shall be based on one digital signature or shall use different digital signature that belongs to the same taxpayer for retailing e-invoice.

- Digital signature is mandatory to present in the e-invoice. The attached sample shows typical digital signature as Issuer's Digital Signature as mandatory field. However, the length of the digital signature is yet to be finalized.

- Quick Response Code QR Code

- QR Code shall include TIN and Seller's Name.

- The SDK shall indicate the development on QR Code whether it is based on Base64 string.

- The SDK shall indicate the contents of QR code in term of Tag, Length and Value (TLV)

- Provision for Data Dictionary - Helpful in XML schema

- The SDK shall provide complete lists of data dictionary as whether it is based on PEPPOL INTERNAITONAL (PINT) or Malaysia specific data field.

- It shall provide UBL XML schema sample to help in the software development and how to fill in from data catalogue published by IRBM.

- Provide sample value in each data field and whether validation will be done during validation stage.

- Provide indication whether the data field is mandatory or optional as not all e-invoices issued contain Sales Tax, Service Tax or Tourism Tax.

- Elaboration on File Storage Path

- IRBM provided the file storage in the e-invoice guideline. Therefore, the software development shall dedicate the folders to store the e-invoices generated before sending for validation and after validation.

- File Name Convention

- The SDK shall indicate the file name for generated e-invoices. The objective is to make sure that no e-invoices with the same file name are sent to IRBM for validation at the same time.

- Typical file name convention as below:

- TIN

- DATETIME

- E-Invoice Code / Number

- Example: C22218888888_20240801151308_INV12345.xml

- Details

- Written by: Administrator

- Category: E-Invoicing

- Hits: 304

E-Invoicing Study: Anticipated Components in Software Development Kit Related to SST Malaysia.

As Malaysia is using Sales Tax and Service Tax as single tier indirect tax without input tax claim, the SDK shall consider issuing additional guideline while adopting Peppol or other standard in the development of E-Invoice. Majority of E-Invoice will not display tax value except SST and Tourism Tax.

The software development kit shall consider of the following sections:

- General Information, Scope, and Development Guidelines

- The SDK shall consist of general information about the purpose, scope, and target audience of this guide. It provides version control as to the changes in the SDK as well as providing a glossary of terms in the document.

- The next valuable piece of information is that the SDK must refer to the legislative documents that empower the development of E-Invoice.

- SDK shall highlight as to what standards to be used. For example, PEPPOL BIS, UBL and Malaysia specified standard related to Sales Tax and Service Tax (SST).

- It shall provide FAQ to address frequent questions to be asked by the audience and contact information for software developers to raise if any clarification is required.

- System Requirements

- The file name of the transmitted e-invoice must be unique so that no two businesses submit the e-invoices with the same file name.

- The file path is to store the cleared invoice and easy reference for the user to locate it

- Semantic definition for each data field stated in the guideline. Whether this is date, number, percentage, text fields etc. The SDK shall address to the maximum length of each data field that is used to keep bulk contents, for instance, invoice number reference for consolidated e-invoice on monthly basis.

- The data field released in the specific guideline shall map to the data dictionary, whether we follow PEPPOL or any other standards.

- QR Code specification can help the software developer to create QR code and is easy for verification purpose.

- Business Processes

- The SDK shall provide complete lists of common business processes that are defined in e-invoice development. For example, a business process requires whether an e-invoice has a valid invoice reference number. Calculation of the price, quantity and discount are correctly at item line as well as sub-total and grand total.

- Since Malaysia is using sales tax and service tax (SST), the SDK shall publish a set of business processes related to SST transactions in Malaysia. As e-invoice may consist of sales tax or service tax exemption, the business rule needs to check whether the exemption certificate is available before the tax value field is calculated as zero instead of tax value.

- The rounding mechanism is also important for quantity, price and total. The SDK shall give an example of how the rounding works.

- Item line total aggregate must be tally with sub-total and grand total.

- Business Validation Rules

- The common business validation rules shall check the semantic data types as date and time, percentage, numeric and text data fields. The business validation rule shall cross-check the validity of NRIC, TIN, BRN and SST ID while it shall not check if it is foreign passport number.

- Other common business validation rules from Peppol and EN 16931 shall also apply to e-invoices. For example, an e-invoice must consist of an invoice reference number.

- The SDK shall publish a set of Malaysia-specified business validation rules such as Sales Tax and Service Tax calculation and sales tax exemption certificate validation.

- Disaster Recovery and Error Handling

- The SDK shall suggest and recommend disaster recovery plans related to blackouts, Internet Unavailability in rural areas, and system failure handling procedures.

- The SDK shall publish the error-handling procedure and reporting related to tax authority portal (MYINVOIS Portal) unavailability.

- Details

- Written by: Administrator

- Category: E-Invoicing

- Hits: 569

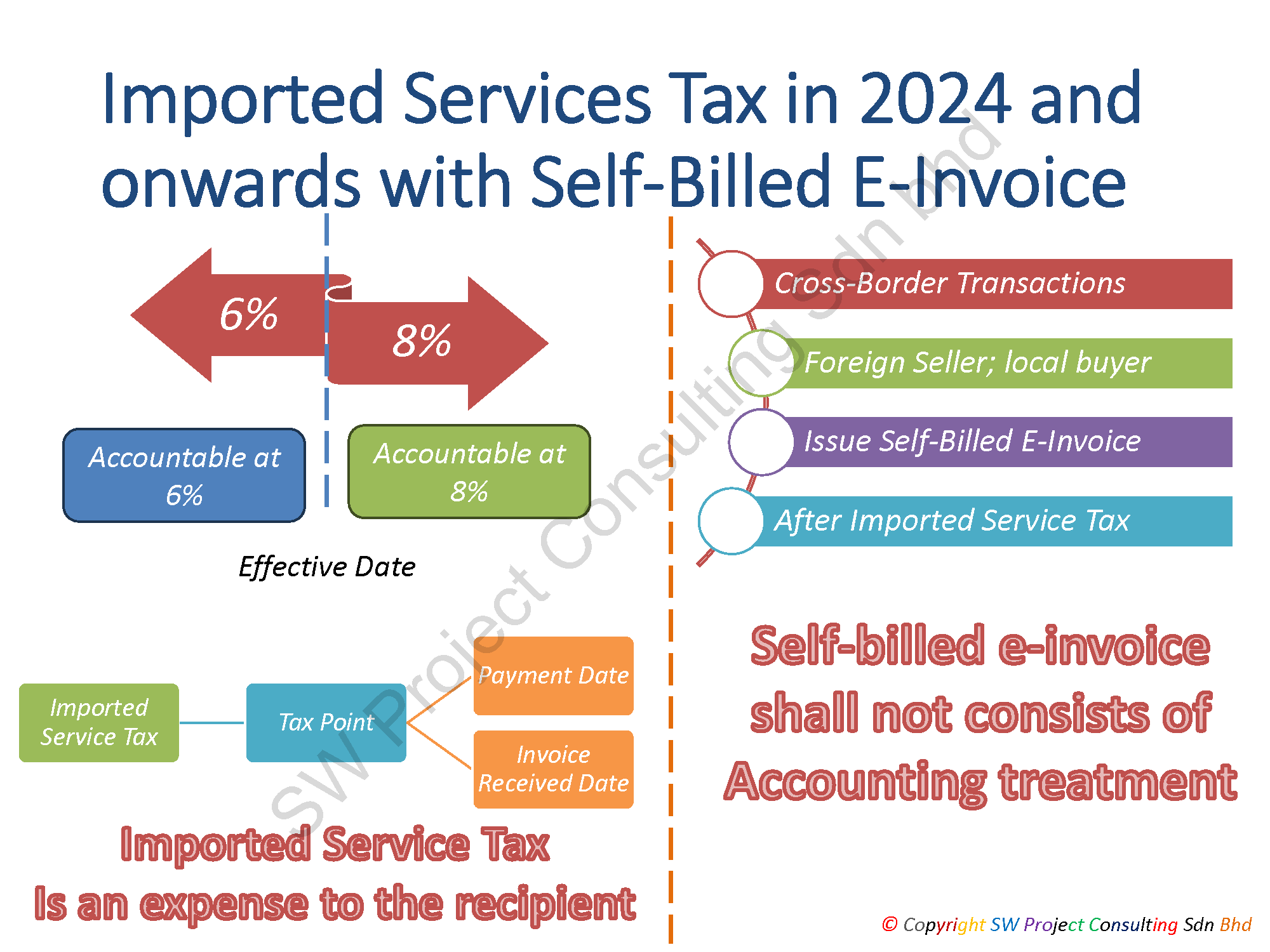

Imported Service Tax in 2024 onwards with Self-Billed E-Invoice

- Malaysia service tax will revise from 6% to 8% in 2024. Any imported taxable service before the effective date is subject to 6% and the tax rate will revise to 8% after effective date.

- Imported service tax in Malaysia is based on the payment date and invoice received date, whichever is earlier.

- Imported service tax is an expense to the recipient

Recipient of imported taxable service must prepare self-billed e-invoice after the payment of imported service tax.

The condition for the self-billed e-invoice as above:

- It is a cross-border transaction

- The recipient is acting as local buyer while foreign seller provides the taxable service, consumable in Malaysia

- To complete Self-Billed E-Invoice, the local buyer will now act as supplier as foreign seller.

- Local buyer as supplier will issue self-billed E-Invoice after the payment of imported service tax.

- There shall be no accounting impact for this self-billed e-invoice for imported taxable service.

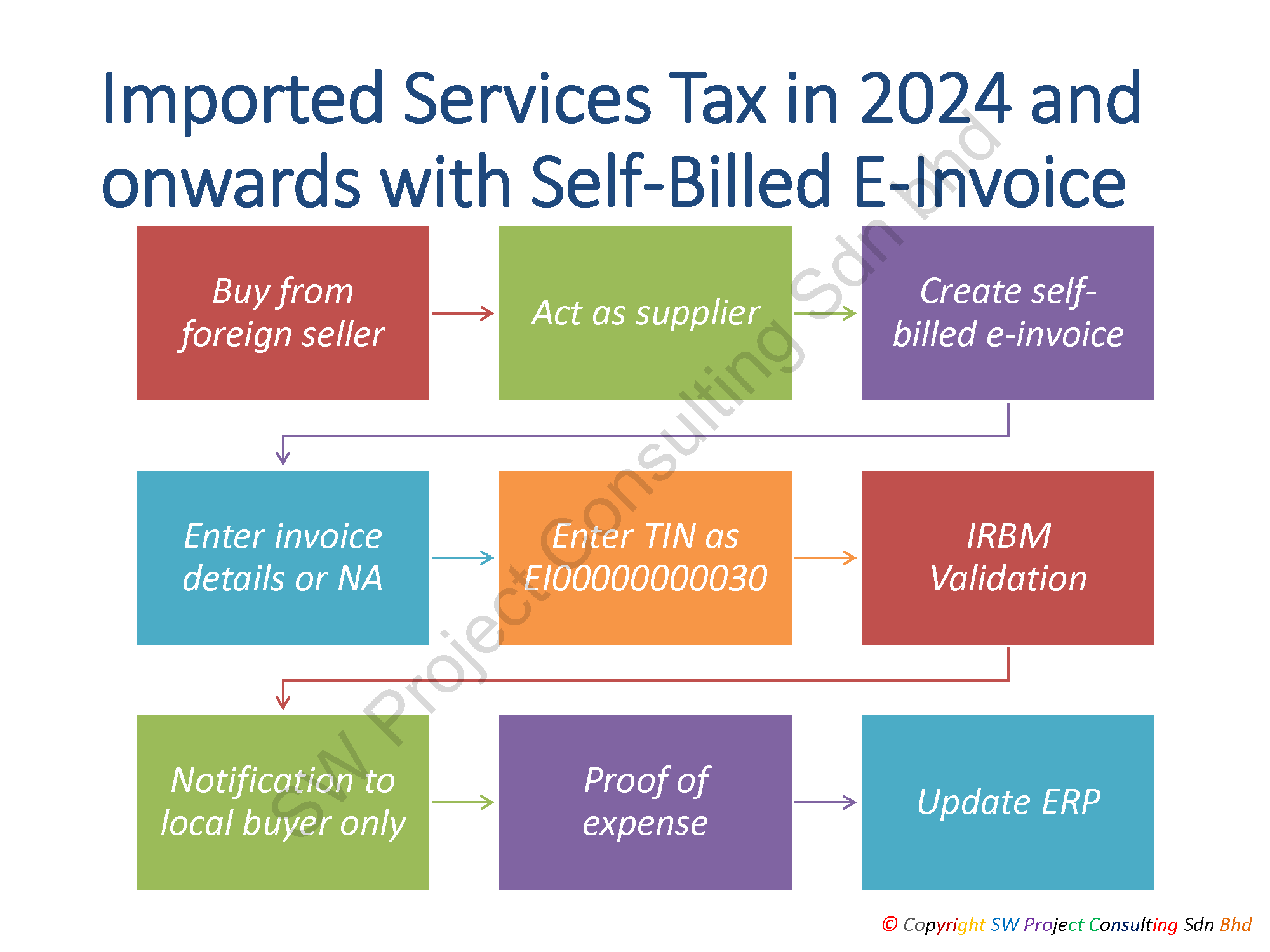

The flow of the self-billed e-invoice as below:

- Local buyer acquires taxable service from overseas service provider and completes payment for imported service tax

- Local buyer will act as supplier to issue self-billed e-invoice

- Local buyer will create self-billed e-invoice

- Local buyer can check with foreign seller for the details to be entered into self-billed e-invoice or enter NA if information is not available

- Local buyer will enter EI0000000030 as TIN - Tax Identification Number in self-billed e-invoice

- Once the e-invoice is created, it will send to IRBM for validation by API or access point

- IRBM will send notification to the local buyer only

- The self-billed e-invoice is viewed as proof of expense for tax purpose

- Local buyer will update or synchronize with ERP or accounting system

- Details

- Written by: Administrator

- Category: E-Invoicing

- Hits: 442

E-Invoicing Study - Gap Assessment for E-Invoicing Implementation

Before E-Invoicing is going to implement in Malaysia in 2024, the organization needs to perform a gap assessment to the current invoicing workflow to determine any procedure changes to accommodate with the E-Invoicing implementation initiative.

Let's look at six areas to address the gap between current process and E-Invoicing process:

- Assessment on ERP, Accounting, Cloud and In-house system: The number of invoicing systems used in the organization. This is to assess the impact of the future direction on whether it shall consolidate into single system for better E-Invoicing operation or remain decentralized to assess the readiness for E-Invoicing integration from different vendors.

- Assessment of the current invoice authorization workflow: This is to assess the current invoice issuing authority so that proper digital signature can be assigned to the right personnel. This is applicable as to the organization using multi-systems and with multi-level authorization to issue and approval invoice. Once the cleared invoice is returned, the organization will consider whether it is still necessary to send PDF invoice to the recipient and archiving options for invoices.

- Assessment of the Internet connection: This is to assess whether invoice generation process needs to be centralized or still decentralized as not all areas will get a strong internet connection. The E-Invoicing validation may post a challenge if the connection with the tax authorization is lagging, slow or disconnected.

- Another assessment in the cybersecurity and firewall: This is to assess the organization firewall can stop cyber-attack from the hackers as to E-Invoices are sent for validation and returned cleared E-invoices to the organization.

- Assessment of customers and vendors data availability: As E-Invoicing will require the master data from the customer such BRN, TIN, SST, MyKad and Passport number. This assessment is to classify data availability of the customers to fit into the organization invoicing generation system. Similarly, the same will apply to the vendors.

- Assessment on budget to conduct workshop and preparation for E-Invoicing implementation: Vendor selection to setup project team and staff training to kick-start E-invoicing implementation.